Get Answers

Understanding Bankruptcy and Eviction in the UK

In the UK, bankruptcy is a legal status that occurs when an individual cannot repay their outstanding debts. While it provides a fresh start by wiping away most debts, it does not necessarily protect against all legal actions, such as eviction. It's crucial for tenants facing eviction while contemplating bankruptcy to grasp how the process may impact their housing situation.

The Process of Filing for Bankruptcy

Filing for bankruptcy in the UK involves submitting a petition to the Insolvency Service, which can be done online or via a paper form. Once bankruptcy is declared, an Official Receiver or an Insolvency Practitioner takes control of the individual's financial affairs. This process is primarily aimed at debt relief and repayment structuring, providing the debtor with a means to manage their financial predicament legally.

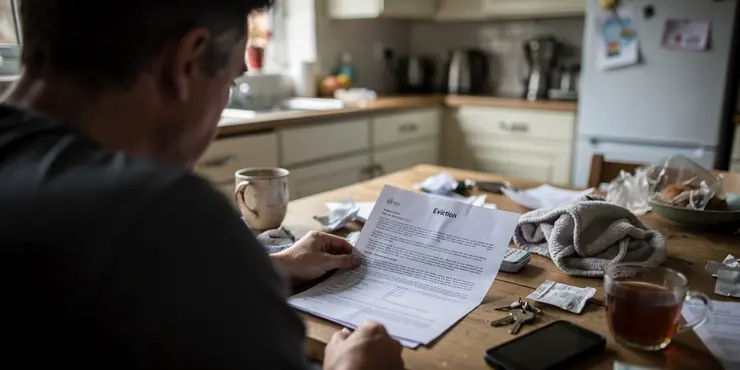

Eviction Process in the UK

The eviction process in the UK generally requires landlords to follow legal procedures, including obtaining a court order. Eviction notices like Section 8 and Section 21 are commonly used in housing disputes. A Section 21 notice allows for possession without the landlord giving a reason, while a Section 8 notice is often used when the tenant has breached the terms of the tenancy agreement, such as failing to pay rent.

Impact of Bankruptcy on Eviction

Filing for bankruptcy does not inherently halt eviction proceedings in the UK. Unlike in some jurisdictions, UK bankruptcy does not automatically freeze eviction actions unless specifically ordered by a court. Landlords with a valid possession order can proceed with eviction after bankruptcy is declared. Tenants should be aware that rent arrears prior to the bankruptcy filing are included in the bankruptcy process, but this does not prevent eviction based on those arrears if a landlord has already initiated legal proceedings.

Secured and Unsecured Debts

In the context of bankruptcy, rent arrears are deemed unsecured debts, which means they are included in the bankruptcy order. However, eviction is a separate legal matter. Even if unpaid rent is written off through bankruptcy, it does not negate the landlord's right to reclaim possession of the property. Conversely, if the landlord holds a mortgage or other security interest over the property, this is considered a secured debt, which bankruptcy does not affect.

Advice and Support

Facing eviction can be distressing, and those experiencing financial difficulty should seek advice from legal or debt counselling services. Organizations such as Citizens Advice, Shelter, and debt charities like StepChange provide guidance on dealing with both bankruptcy and eviction. It's recommended to obtain professional advice tailored to individual circumstances as responses to eviction notices and bankruptcy alternatives can vary based on specific legal contexts.

Conclusion

In conclusion, while bankruptcy provides a means to manage overwhelming debts in the UK, it does not automatically stop the eviction process. Tenants at risk of eviction must address both their financial and housing issues separately, ensuring they take appropriate legal actions and seek expert advice where necessary.

Understanding Bankruptcy and Eviction in the UK

In the UK, if you cannot pay your debts, you might declare bankruptcy. Bankruptcy means you get a chance to start over, and many debts are erased. But, it does not stop all actions, like being evicted from your home. If you are a tenant and worried about being evicted while thinking about bankruptcy, it’s important to understand how this might affect your home situation.

The Process of Filing for Bankruptcy

To file for bankruptcy in the UK, you fill out a form online or on paper and send it to the Insolvency Service. Once you declare bankruptcy, an Official Receiver or Insolvency Practitioner will help manage your money. This process helps you deal with your debts in a legal way.

Eviction Process in the UK

In the UK, landlords must follow the law to evict you. They need a court order to do it. Landlords often use Section 8 or Section 21 notices. A Section 21 notice means they want you to leave without giving a reason. A Section 8 notice is used if you have broken the rules of your rental agreement, like not paying rent.

Impact of Bankruptcy on Eviction

Declaring bankruptcy in the UK does not stop eviction by itself. Your landlord can still try to evict you even if you are bankrupt. If your landlord already started legal eviction steps before you declared bankruptcy, they can continue after. Any rent you didn’t pay before bankruptcy is considered by the bankruptcy, but your landlord can still evict you for these unpaid rents if they have a court order.

Secured and Unsecured Debts

In bankruptcy, unpaid rent is called unsecured debt, which means it gets included in the bankruptcy order. However, eviction is a separate issue. Even if your unpaid rent is erased, the landlord can still ask you to leave the property. But, if there’s a mortgage on your home, it’s a secured debt and not affected by bankruptcy.

Advice and Support

If you are worried about eviction, it is important to get help. You can talk to legal or debt help services. Groups like Citizens Advice, Shelter, and charities like StepChange can give you advice about bankruptcy and eviction. Get advice that fits your situation because dealing with eviction and bankruptcy can be different for each person.

Conclusion

In summary, bankruptcy in the UK helps with debts, but it does not stop eviction automatically. Tenants facing eviction should deal with both money and housing problems separately. It is important to take the right legal steps and ask for expert advice if needed.

Frequently Asked Questions

Bankruptcy is a legal process that provides relief to individuals or businesses that are unable to pay their debts.

Filing for bankruptcy may temporarily stop an eviction due to the automatic stay, but it depends on the circumstances of the eviction.

An automatic stay is a legal provision that immediately stops most collection actions, including evictions, once a bankruptcy case is filed.

No, the automatic stay may not apply if the landlord has already obtained a judgment for possession or if the eviction is due to illegal activity.

The automatic stay lasts for the duration of the bankruptcy proceedings unless the court grants a motion for relief from the stay.

Yes, a landlord can file a motion for relief from the automatic stay to continue with eviction proceedings.

If a landlord gets relief from the automatic stay, they can proceed with the eviction process.

Bankruptcy can discharge certain debts, but rent arrears are usually not discharged in Chapter 7 bankruptcy.

Filing for Chapter 13 bankruptcy might help stop eviction by allowing you to include rent arrears in your repayment plan.

Yes, bankruptcy can have long-term effects on your credit and does not guarantee eviction prevention.

It is important to consult with a bankruptcy attorney to understand your rights and options.

No, evictions based on illegal drug use or endangerment are not protected by the automatic stay.

State laws can vary, affecting how bankruptcy impacts eviction, so it’s essential to consult with legal counsel.

Chapter 13 repayment plans can include past rent arrears but typically don't cover ongoing rent obligations.

A bankruptcy trustee oversees your case but does not directly intervene in eviction matters.

Alternatives include negotiating with your landlord, seeking rental assistance programs, or exploring payment arrangements.

Filing bankruptcy can affect your credit score and rental history, which may impact your ability to rent in the future.

You will need to provide financial documentation, including assets, debts, income, and expenses.

Bankruptcy can potentially discharge other unsecured debts related to housing, such as utility bills.

A Chapter 7 bankruptcy can stay on your credit report for up to 10 years, while a Chapter 13 can stay for up to 7 years.

Bankruptcy is a way the law can help people or businesses that cannot pay back the money they owe.

When you file for bankruptcy, it might pause an eviction for a short time. This is called an automatic stay, but it may not work in every eviction situation.

An automatic stay is a rule that helps people. When someone asks for bankruptcy, it makes most actions to collect debts stop right away. This includes stopping evictions.

No, the automatic stop might not work if the landlord already has a court order saying you have to leave your home, or if the eviction is because of something against the law.

The automatic stop lasts while the bankruptcy case is happening. But, it can end early if the court says it's okay.

Yes, a landlord can ask the court to let them keep going with an eviction, even if there is a rule stopping them for now.

If a landlord gets allowed by a court to go forward, they can start the process to make a tenant move out.

Bankruptcy can help get rid of some debts. But money owed for rent usually isn't wiped away when you use Chapter 7 bankruptcy.

Chapter 13 bankruptcy is about managing money when you have debts. It can help stop eviction by letting you pay back missed rent in a plan. This plan helps you catch up on what you owe.

Yes, if you declare bankruptcy, it can harm your credit for a long time, and it won't always stop you from being evicted.

It is good to talk to a lawyer about bankruptcy. They can help you know what you can do and what your choices are.

No, if someone is being removed from their home for using illegal drugs or being dangerous, the automatic rule that stops evictions does not protect them.

Different places have different rules. These rules can change how bankruptcy affects eviction. It’s important to talk to a lawyer to understand what could happen.

Chapter 13 plans can help pay back old rent. But you still need to pay your new rent every month.

A bankruptcy helper takes care of your case, but they do not help with getting you out of a home.

Here are some ways to get help:

- Talk to your landlord and try to make a new deal.

- Look for programs that help pay rent.

- See if you can make a payment plan.

Filing for bankruptcy can change your credit score. This might make renting a home harder in the future.

You need to share some money information. This includes what you own, what you owe, the money you make, and the money you spend.

Bankruptcy might help you get rid of other debts that are not backed by anything, like money owed for gas, electricity, and water bills.

A Chapter 7 bankruptcy can stay on your credit report for 10 years. A Chapter 13 can stay for 7 years.

Here are some tools that might help:

- Use a calendar to track the time.

- Set reminders on your phone.

- Ask a family member or friend to help you remember.

Ergsy Search Results

This website offers general information and is not a substitute for professional advice.

Always seek guidance from qualified professionals.

If you have any medical concerns or need urgent help, contact a healthcare professional or emergency services immediately.

Some of this content was generated with AI assistance. We've done our best to keep it accurate, helpful, and human-friendly.

- Ergsy carefully checks the information in the videos we provide here.

- Videos shown by Youtube after a video has completed, have NOT been reviewed by ERGSY.

- To view, click the arrow in centre of video.

- Most of the videos you find here will have subtitles and/or closed captions available.

- You may need to turn these on, and choose your preferred language.

- Go to the video you'd like to watch.

- If closed captions (CC) are available, settings will be visible on the bottom right of the video player.

- To turn on Captions, click settings.

- To turn off Captions, click settings again.