Speak To An Expert

Get clear, personalised advice for your situation.

Jot down a few questions to make the most of your conversation.

More Items From Ergsy search

-

How much can I borrow for a mortgage UK - getting the Maximum Mortgage

Relevance: 100%

-

Getting the maximum mortgage in the UK

Relevance: 99%

-

Mortgage Regulator removes the need for further affordability stress tests

Relevance: 83%

-

The Ultimate Buy-To-Let Mortgage Breakdown

Relevance: 75%

-

What is an 'interest only' mortgage?

Relevance: 74%

-

Uk Buy to Let for Older Clients - Mortgage Options Tips and Criteria

Relevance: 70%

-

Mortgage Overpayment and Flexible Features Explained

Relevance: 68%

-

Mortgage Turned Down In The UK - Why mortgage applications are declined

Relevance: 68%

-

Highest Income Multiple Mortgage Lenders Revealed - Good and Bad Points

Relevance: 68%

-

What is a tracker mortgage and how does it respond to interest rate changes?

Relevance: 68%

-

Using 100% of your Second Income for a Mortgage Application

Relevance: 68%

-

UK Mortgage Rules Lenders Don't Talk About - Debt To Income Ratio

Relevance: 67%

-

How do interest rate changes affect my mortgage payments?

Relevance: 66%

-

What should I do if I can't afford my mortgage payments due to rising interest rates?

Relevance: 66%

-

Selecting a Mortgage Broker - how they differ and what to watch out for

Relevance: 66%

-

Turned down for a mortgage? Find out why and what to do

Relevance: 65%

-

What does it mean to "Fix My Mortgage Rate"?

Relevance: 64%

-

5 Broker Exclusive Buy to Let Mortgage Lenders you need to know about as a Landlord

Relevance: 64%

-

Can Stamp Duty be included in a mortgage in the UK?

Relevance: 64%

-

First Time Buyer Buy to Let Finance Options. Lending Criteria on Mortgage and Bridging Finance

Relevance: 64%

-

Is a mortgage valuation the same as a surveyor's report?

Relevance: 63%

-

Mortgage on Inherited Property - How we can help you with the finance

Relevance: 62%

-

Will my fixed-rate mortgage payments change with interest rate fluctuations?

Relevance: 62%

-

HMO Mortgage Truths - how to get the best Finance option including Bridging Loan Criteria

Relevance: 61%

-

RIGHT TO BUY MORTGAGE - LET ME SAVE YOU TIME AND MONEY

Relevance: 61%

-

Can I get a Buy to Let Mortgage With My 18 Year Old Son

Relevance: 61%

-

First Time Buyer Buy to Let Finance Options. Lending Criteria on Mortgage and Bridging Finance

Relevance: 60%

-

Is it possible to switch my mortgage type if interest rates become unfavourable?

Relevance: 60%

-

Turned down for a mortgage? Find out why and what to do

Relevance: 58%

-

Can I use the surveyor recommended by my mortgage provider?

Relevance: 58%

-

Is there assistance available for rent or mortgage payments?

Relevance: 58%

-

Can Mortgage lenders work from my own Survey Valuation Report?

Relevance: 57%

-

How to Buy property with your children under the age of 18 and get Buy to Let Mortgage.

Relevance: 52%

-

Are first-time buyers affected differently by interest rate changes?

Relevance: 49%

-

Should you Pay down your Residential Mortgage?

Relevance: 48%

-

What is an SVR and how does it relate to interest rate changes?

Relevance: 44%

-

Remortgage within 6 Months on the open market value Residential or Buy to Let Properties

Relevance: 44%

-

Major Banks Announce Changes in Interest Rates: Are You Affected?

Relevance: 42%

-

What happens to my monthly payments if interest rates rise?

Relevance: 38%

-

House Prices Soar: First-Time Buyers Share Their Stories

Relevance: 37%

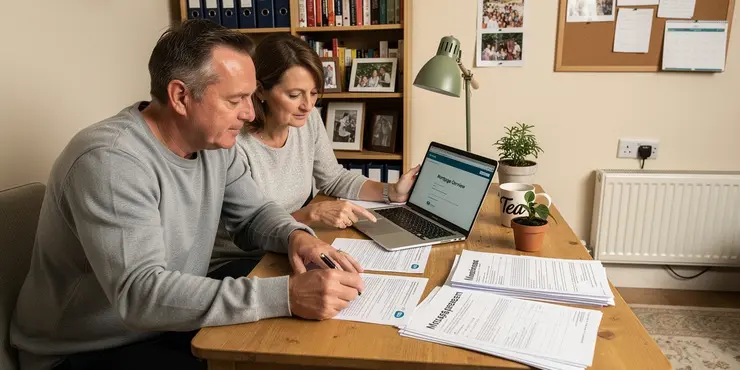

How Much Can I Borrow for a Mortgage in the UK?

Buying a home is a major financial commitment, and understanding how much you can borrow is crucial in planning your property purchase. In the UK, the amount you can borrow for a mortgage depends on several factors, including your income, credit history, and current debts. This guide will provide an overview of these factors and how you can maximise your mortgage borrowing potential.

Understanding Your Income and Affordability

Your income is one of the primary determinants of how much you can borrow. Lenders typically use a multiple of your income to calculate the maximum mortgage amount. This is often between three to five times your annual income. For joint applications, many lenders will consider joint incomes and may apply the multiple to the total combined income. It's important to also consider your monthly expenses and any existing debts, as these will impact your affordability checks. Lenders will perform stress tests to ensure you can afford repayments even if interest rates rise.

The Role of Credit History and Score

Your credit history will significantly impact how much you can borrow. A strong credit score reflects a history of meeting financial obligations on time, and as such, it might allow you to secure a higher loan amount at better interest rates. Poor credit history could limit your borrowing options or require you to pay a higher interest rate. Before applying for a mortgage, it’s advisable to check your credit score and address any issues to improve your borrowing prospects.

Maximising Your Mortgage Potential

To increase your borrowing potential, consider taking steps such as boosting your deposit amount, which not only reduces the loan amount needed but also can give you access to better mortgage deals. Seeking financial advice from a mortgage broker can also be beneficial, as they can provide insights on navigating complex situations and identifying lenders who might extend more favourable terms. Additionally, reducing outstanding debts, managing spending, and improving your credit score are effective strategies for enhancing affordability and mortgage limits.

Keep in mind specific schemes like the Help to Buy scheme, or the Shared Ownership plan which might affect how much you can borrow depending on your circumstances. Always conduct thorough research and consult with a financial advisor to understand the best approach for your situation.

How Much Can I Borrow for a Mortgage in the UK?

Buying a home is a big decision. It's important to know how much money you can borrow to buy a house. In the UK, this depends on things like your income, your credit history, and any money you already owe. This guide will help you understand these things and how you can borrow the most money possible.

Understanding Your Income and Affordability

Your income, or how much money you make, is very important for borrowing. Banks look at your income to see how much you can borrow. They often allow you to borrow three to five times your yearly income. If you are buying a house with someone else, they might add your incomes together. You also need to think about your monthly bills and any money you owe, because those affect how much you can afford to borrow. Banks check to see if you can still pay if interest rates go up.

The Role of Credit History and Score

Your credit history is about how well you have paid back money in the past. A good credit score means you have paid on time, and this can help you borrow more money with better interest rates. If you have a bad credit history, it can make borrowing harder or more expensive. It's a good idea to check your credit score before asking for a mortgage and fix any problems. This can help you borrow more money.

Maximising Your Mortgage Potential

To borrow more money, you can do a few things. Saving up a bigger deposit can reduce how much you need to borrow and help you get better deals. Talking to a mortgage broker can also help you find the best options. Paying off any debts, managing your spending, and improving your credit score can also help you borrow more and get better terms.

There are also special plans like Help to Buy or Shared Ownership that might help, depending on your situation. Always research and maybe talk to a financial advisor to find the best way for you to get a mortgage.

Frequently Asked Questions

How is my mortgage borrowing limit determined in the UK?

In the UK, your mortgage borrowing limit is typically determined by multiplying your annual income by a certain factor, usually between 3 to 4.5 times, depending on the lender. Factors such as your credit score, existing debts, and overall financial situation can also impact this.

What factors do lenders consider when assessing how much I can borrow?

Lenders consider your income, expenses, credit history, existing debts, the interest rate type, and the size of the deposit you can make. Stability of income and employment type can also influence lending decisions.

How does my credit score affect my mortgage borrowing capacity?

A higher credit score often allows you to borrow more because it signals to lenders that you are likely to repay the loan on time. A low credit score could limit your borrowing capacity and result in higher interest rates.

Can I borrow more with a larger deposit?

Yes, a larger deposit can increase your borrowing power because it reduces the lender's risk. Additionally, larger deposits can also lead to more favorable interest rates and mortgage terms.

What is a loan-to-value (LTV) ratio and how does it affect my mortgage?

The loan-to-value (LTV) ratio is the amount you borrow compared to the value of the property, expressed as a percentage. A lower LTV ratio often results in better interest rates, as there is less risk for the lender.

How does my employment status affect my mortgage application?

Lenders prefer applicants who have stable employment and regular income. Being self-employed or having irregular income can make the mortgage process more challenging, but providing detailed financial records can help.

Are there any schemes in the UK to help first-time buyers maximize their mortgage?

Yes, the UK government offers schemes such as Help to Buy and shared ownership, which can help first-time buyers get on the property ladder with a smaller deposit and potentially maximize their mortgage.

Can existing debts impact the amount I can borrow?

Yes, existing debts are taken into account when assessing your affordability. Higher existing debts can reduce the amount you are able to borrow because they affect your debt-to-income ratio.

Will I need to pay any upfront fees when applying for a mortgage?

Yes, there may be upfront costs such as arrangement fees, valuation fees, and legal costs. These can vary depending on the lender and specific mortgage product.

How can I improve my chances of getting the maximum mortgage?

To improve your chances, maintain a good credit score, reduce existing debts, save for a larger deposit, and provide evidence of a stable income and employment history.

What role does interest rate play in determining how much I can borrow?

A lower interest rate often means you can afford a larger mortgage, as your monthly repayments will be lower. Conversely, higher rates can reduce borrowing capacity.

Are there any online tools to estimate how much I can borrow?

Yes, most lenders offer online mortgage calculators where you can input your income, expenses, and other financial details to get an estimate of how much you can borrow.

What is a mortgage in principle and does it guarantee I can borrow that amount?

A mortgage in principle offers an estimate from a lender on how much they might lend you, based on your financial situation. It's not a guarantee, as the final amount will depend on a full application assessment.

If interest rates rise, how will this impact the amount I can borrow?

Rising interest rates generally mean higher repayments, which could reduce the amount you are able to borrow. Lenders will stress-test applicants to ensure they can afford rate increases.

Can I still borrow if I have a poor credit history?

It might be more challenging to secure a mortgage with a poor credit history, but there are lenders who specialize in offering 'bad credit' mortgages. These often come with higher interest rates and stricter terms.

How do people in the UK decide how much money I can borrow for a house?

In the UK, how much money you can borrow for a house (called a mortgage) depends on how much money you make each year. The bank usually lets you borrow 3 to 4.5 times your yearly income. But things like your credit score (how good you are at paying back money), any other money you owe, and your overall money situation can change this amount.

If you find this hard to understand, you can use tools that help explain money. They have pictures and simple words. You can also ask someone to explain it to you with easy words.

What do banks think about when they decide how much money I can borrow?

When you want to borrow money, like for a house, lenders look at a few important things. They check how much money you make and how much you spend. They also see if you have borrowed money before and if you have paid it back on time. They look at any other money you owe too.

Lenders also think about how much money you can pay upfront. They check if your job is steady and how you earn your money. All these help them decide if they can lend you money.

If reading is hard for you, try using a reading pen or ask someone to read with you. You can also listen to audiobooks to understand better.

How does my credit score affect my mortgage borrowing capacity?

Your credit score is a number that shows how good you are at paying back money you borrow.

If you have a high credit score, it means you usually pay back money on time. This can help you borrow more money, like for a house (this is called a mortgage).

If your credit score is low, it might be harder to borrow money. You might not be able to borrow as much, or you might have to pay more money back.

Some people find it helpful to use a calculator or a money app to keep track of their payments.

A good credit score means you can borrow more money because banks trust you to pay it back. If your credit score is low, you might not be able to borrow as much, and you might have to pay more money in interest.

To help manage your money better, you can use a budget planner. This helps you see how much money you earn and spend. Also, setting up reminders to pay bills on time can improve your credit score. Apps on your phone can be useful for this.

If I put down more money, can I borrow more?

Sometimes, if you pay more money upfront, the bank might let you borrow even more money. It's a good idea to ask the bank to make sure.

Helpful Tips:

- Ask someone you trust to explain things to you.

- Use a calculator to see how much you can pay.

- Write down questions you want to ask the bank.

Yes, saving up more money to pay as a deposit can help you borrow more. This is because it makes the bank feel safer. If you pay more deposit, the bank might give you better interest rates and better mortgage deals too.

What is a loan-to-value (LTV) ratio and how does it affect my mortgage?

A loan-to-value ratio, or LTV, is a way to compare a loan with the value of something you buy.

When you get a mortgage to buy a home, the LTV shows how much of the home's price you are borrowing.

For example, if a house costs $100, and you borrow $80, your LTV is 80%.

A lower LTV is usually better. It means you have more money already, and banks like that.

A high LTV might mean higher payments each month, or it can be harder to get the loan.

Remember to ask for help if you're not sure. Talking to a mortgage expert can be a good idea.

- Use Tools: You can use a calculator to understand LTV better.

- Get Support: Ask a family member or friend to read it with you.

The loan-to-value (LTV) ratio is how much money you borrow compared to how much the property is worth. This is shown as a percentage. If the LTV ratio is low, you usually get better interest rates. This is because it's less risky for the lender.

How does my job affect my mortgage application?

Your job can change how you get a mortgage. A mortgage is like a big loan to help you buy a house.

If you have a full-time job, it may be easier to get a mortgage. Lenders like to see that you have money coming in every month.

If you have a part-time job or different jobs now and then, getting a mortgage might be harder. Lenders want to know you can pay them back.

If you are self-employed, like if you run your own business, you might need to show more papers to prove your income.

Here are some tips to help:

- Get all your job papers together, like your payslips or tax returns.

- Use a calculator to see how much you can pay each month.

- Talk to a mortgage advisor. They can explain what you need to do.

Remember, having a stable job helps, but there are always ways to work things out. Good luck!

People who lend money like it when you have a steady job and regular pay. If you work for yourself or your pay changes a lot, getting a home loan might be harder. But if you show them clear records of your money, it can help you a lot.

Are there ways to help first-time home buyers with their mortgage in the UK?

Yes, there are ways to help people buying a home for the first time in the UK.

These are some helpful ways:

- Help to Buy: The government can help you buy a new home.

- Shared Ownership: You can buy part of a home and pay rent on the rest.

- Lifetime ISA: You can save money and get extra money from the government to buy your first home.

If you find reading hard, you can try:

- Using a tool to read out the words.

- Asking someone to explain the words to you.

Yes, the UK government has programs that can help people buy their first home. Some of these programs are called Help to Buy and shared ownership. They help people who are buying a home for the first time. With these programs, you might need to pay less money up front to buy a home, and you might be able to borrow more money to buy the home.

Can my current debts change how much I can borrow?

If you owe money now, it might change how much more money you can borrow.

Here are some tools that can help:

- Use a calculator to see how much you owe.

- Talk to a bank to get advice on borrowing money.

- Make a list of all the money you owe and try to pay some off.

Yes, if you already owe money, it can change how much money you can borrow. If you owe a lot, you might not be able to borrow much more. This is because it changes how much money you have compared to how much you owe.

Do I need to pay any money when I apply for a mortgage?

When you ask for a mortgage, you might need to pay some money first. This is called an 'upfront fee'.

Here are a few tips to help:

- Talk to a bank or lender. They can explain the fees.

- Ask someone you trust to help you understand.

- Use a calculator online to see costs.

Yes, there might be costs at the start, like setup fees, checking the house value, and lawyer costs. These can be different for each money lender and mortgage plan you pick.

How can I get the biggest home loan?

If you want to borrow as much money as possible to buy a house, here are some easy tips to help:

- Save Money: Try to save more money for a bigger deposit. This can help you borrow more.

- Pay Bills on Time: Paying all your bills on time can make your credit score better. A better score can help you get a bigger loan.

- Earn More Money: If possible, try to increase your income. More money can help you borrow more.

- Debt Check: Try not to have too much debt. Less debt can help you get a bigger loan.

Helpful Tools: Use a calculator to see how much you can borrow. You can find these calculators online.

If you want a better chance, keep a good credit score. Try to pay off any money you owe. Save up for a bigger deposit. Also, show proof that you have a stable job and income.

How do interest rates affect the amount I can borrow?

Interest rates are like extra costs you pay when you borrow money. They are important because:

- If interest rates are low, you can usually borrow more money.

- If interest rates are high, you might not be able to borrow as much.

You can use tools like calculators to help understand how interest rates work. You can also ask a trusted adult or financial advisor to explain it to you.

When the interest rate is low, it means you can borrow more money to buy a house because the payments each month will be smaller. But, if the interest rate is high, you might not be able to borrow as much money.

Can I use online tools to see how much money I can borrow?

Yes, many banks have online calculators. You can use these to see how much money you might be able to borrow for a house. You just need to type in your income (the money you earn), your expenses (the money you spend), and other money details.

What is a Mortgage in Principle and Does it Mean I Can Borrow That Money?

A mortgage in principle is a letter from a bank or lender saying how much money they might let you borrow to buy a house.

But it does not mean you will definitely get that money later.

To understand more, you can ask questions or use tools that help explain things better, like talking to someone who knows about mortgages.

A mortgage in principle is like a promise from a bank about how much money they might let you borrow to buy a house. They use your money details to guess this amount. But remember, it's not for sure! The real amount might be different when they check everything.

If interest rates go up, how will this change the amount I can borrow?

Interest rates are like extra money you pay when you borrow money. If these rates go up, it might mean you can borrow less money. This is because you have to pay more extra money back.

When interest rates go up:

- You might have to pay more each month.

- You might not be able to borrow as much.

Here are some tips to help you understand better:

- Ask a family member or a friend to explain it to you.

- Use a calculator to see how much you can borrow.

When interest rates go up, it usually means you have to pay back more money. This might mean you can borrow less money from the bank. Banks check to make sure you can still pay back the money if the rates go up.

Can I get a loan if I have bad credit?

If you have bad credit, you might still be able to borrow money. Here is what you can do:

- Check your credit score: Look at your credit report to see what it says.

- Talk to a bank or lender: Ask them what options you have.

- Find a co-signer: Ask someone with good credit to help you get a loan.

- Think about a secured loan: This means you promise to give something valuable if you can't pay back the loan.

Using these ideas might help you borrow money, even if your credit is not good.

If reading is hard, ask someone you trust to explain this to you.

Getting a home loan with bad credit can be hard. But some banks help people with bad credit. These loans might cost more money, and the rules can be tougher.

Useful Links

This website offers general information and is not a substitute for professional advice.

Always seek guidance from qualified professionals.

If you have any medical concerns or need urgent help, contact a healthcare professional or emergency services immediately.

Some of this content was generated with AI assistance. We've done our best to keep it accurate, helpful, and human-friendly.

- Ergsy carefully checks the information in the videos we provide here.

- Videos shown by Youtube after a video has completed, have NOT been reviewed by ERGSY.

- To view, click the arrow in centre of video.

- Most of the videos you find here will have subtitles and/or closed captions available.

- You may need to turn these on, and choose your preferred language.

- Go to the video you'd like to watch.

- If closed captions (CC) are available, settings will be visible on the bottom right of the video player.

- To turn on Captions, click settings.

- To turn off Captions, click settings again.

More Items From Ergsy search

-

How much can I borrow for a mortgage UK - getting the Maximum Mortgage

Relevance: 100%

-

Getting the maximum mortgage in the UK

Relevance: 99%

-

Mortgage Regulator removes the need for further affordability stress tests

Relevance: 83%

-

The Ultimate Buy-To-Let Mortgage Breakdown

Relevance: 75%

-

What is an 'interest only' mortgage?

Relevance: 74%

-

Uk Buy to Let for Older Clients - Mortgage Options Tips and Criteria

Relevance: 70%

-

Mortgage Overpayment and Flexible Features Explained

Relevance: 68%

-

Mortgage Turned Down In The UK - Why mortgage applications are declined

Relevance: 68%

-

Highest Income Multiple Mortgage Lenders Revealed - Good and Bad Points

Relevance: 68%

-

What is a tracker mortgage and how does it respond to interest rate changes?

Relevance: 68%

-

Using 100% of your Second Income for a Mortgage Application

Relevance: 68%

-

UK Mortgage Rules Lenders Don't Talk About - Debt To Income Ratio

Relevance: 67%

-

How do interest rate changes affect my mortgage payments?

Relevance: 66%

-

What should I do if I can't afford my mortgage payments due to rising interest rates?

Relevance: 66%

-

Selecting a Mortgage Broker - how they differ and what to watch out for

Relevance: 66%

-

Turned down for a mortgage? Find out why and what to do

Relevance: 65%

-

What does it mean to "Fix My Mortgage Rate"?

Relevance: 64%

-

5 Broker Exclusive Buy to Let Mortgage Lenders you need to know about as a Landlord

Relevance: 64%

-

Can Stamp Duty be included in a mortgage in the UK?

Relevance: 64%

-

First Time Buyer Buy to Let Finance Options. Lending Criteria on Mortgage and Bridging Finance

Relevance: 64%

-

Is a mortgage valuation the same as a surveyor's report?

Relevance: 63%

-

Mortgage on Inherited Property - How we can help you with the finance

Relevance: 62%

-

Will my fixed-rate mortgage payments change with interest rate fluctuations?

Relevance: 62%

-

HMO Mortgage Truths - how to get the best Finance option including Bridging Loan Criteria

Relevance: 61%

-

RIGHT TO BUY MORTGAGE - LET ME SAVE YOU TIME AND MONEY

Relevance: 61%

-

Can I get a Buy to Let Mortgage With My 18 Year Old Son

Relevance: 61%

-

First Time Buyer Buy to Let Finance Options. Lending Criteria on Mortgage and Bridging Finance

Relevance: 60%

-

Is it possible to switch my mortgage type if interest rates become unfavourable?

Relevance: 60%

-

Turned down for a mortgage? Find out why and what to do

Relevance: 58%

-

Can I use the surveyor recommended by my mortgage provider?

Relevance: 58%

-

Is there assistance available for rent or mortgage payments?

Relevance: 58%

-

Can Mortgage lenders work from my own Survey Valuation Report?

Relevance: 57%

-

How to Buy property with your children under the age of 18 and get Buy to Let Mortgage.

Relevance: 52%

-

Are first-time buyers affected differently by interest rate changes?

Relevance: 49%

-

Should you Pay down your Residential Mortgage?

Relevance: 48%

-

What is an SVR and how does it relate to interest rate changes?

Relevance: 44%

-

Remortgage within 6 Months on the open market value Residential or Buy to Let Properties

Relevance: 44%

-

Major Banks Announce Changes in Interest Rates: Are You Affected?

Relevance: 42%

-

What happens to my monthly payments if interest rates rise?

Relevance: 38%

-

House Prices Soar: First-Time Buyers Share Their Stories

Relevance: 37%